WELCOME TO THE CLIP!

This is our new bi-weekly newsletter where we do a deep dive into a digital commerce topic. Each issue is a unique and timely analysis, never a regurgitation of news. This analysis goes out to our contact list including public/private companies, venture, and private equity investors, and other participants in the digital commerce sector. Our inaugural issue takes a close look at digitally native vertical brands and capital raising efforts in the sector.

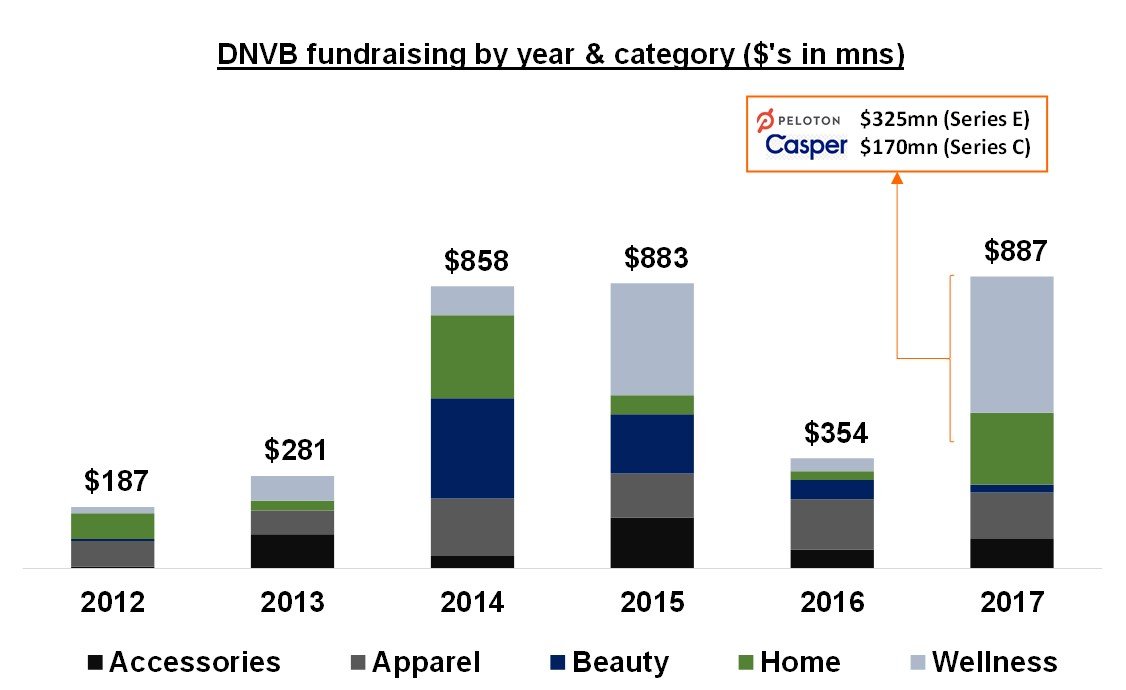

DNVBs have raised ~$900mn this year – but the market is not as healthy as it appears

It was recently reported that John Hancock Investments and several other mutual funds marked down their investments in Warby Parker to a much lower valuation than the previous round so we decided to take a look at the funding environment for digitally native brands.

The term digitally native vertical brand (DNVB) was coined by Andy Dunn, CEO of the recently acquired men’s apparel company Bonobos. DNVB’s continues to disrupt the B2C market and we are tracking more than 300+ companies in this sector with a focus on 5 separate categories: Accessories, Apparel, Beauty, Home, and Wellness. Of these, there are 110 companies that have raised private capital with data reported into various databases including Crunchbase and CapIQ. 2014 and 2015 were boom years for DNVB’s raising between $800-900mn in both years, only to get cut in half in 2016 as tech VCs backed off of the gas after a general lack of eCommerce exits and Amazon fears. Although this year looks like a return to boom times, it might be slightly misleading and look to be more in line with 2016. Year-to-date funding is around $900mn and should break $1bn by year-end but there have been several large rounds that inflate the numbers including Peloton’s enormous $325mn round in May and Casper’s $170mn round in mid-June, boosting both the Home and Wellness categories. The bottom line is that excluding these outliers, 2017 doesn’t look much better than 2016.

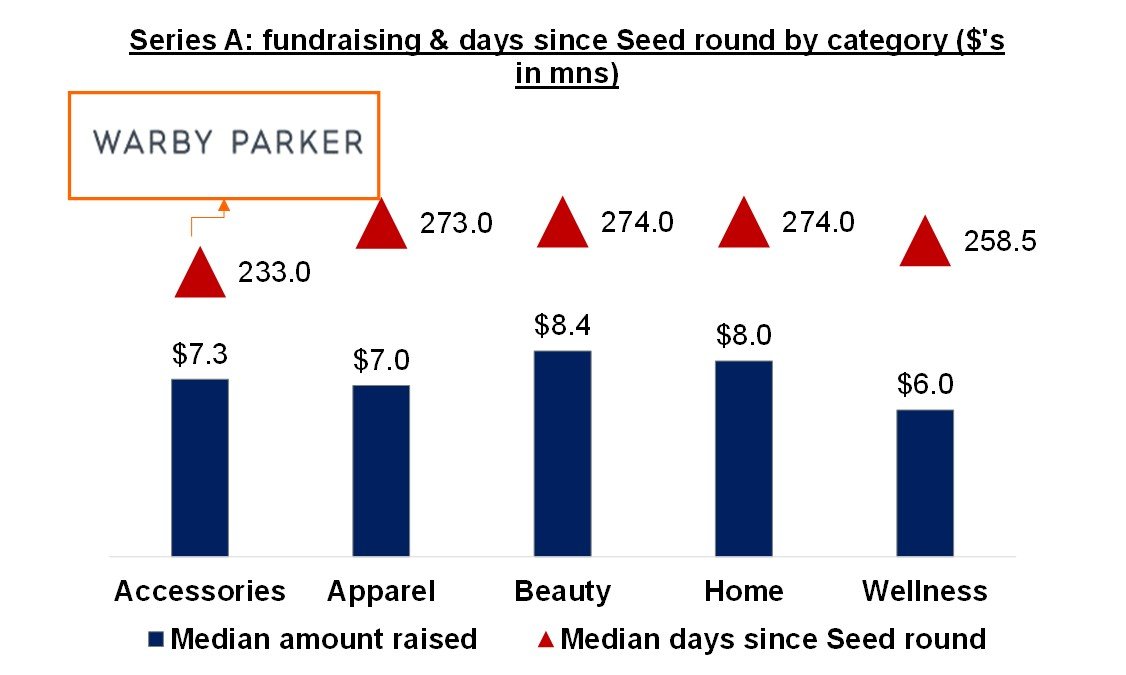

DNVB’s raises every ~330 days

We took a deeper dive to look at DNVB fundraising activity, specifically how much have companies raised from Seed through Series C, and how often do they raise? DNVBs in the apparel and home category raised around 1x per year. While DNVBs in the accessory category raised funds more frequently at a median of every 253 days.

Taking a more granular look by round for Series A financing, DNVBs across all categories raised around $7-$8 million. Accessory DNVBs graduating from Seed to a Series A came in at the lowest time between their next raise of every 233 days, with Warby Parker completing a Series A round 78 days after their Seed round. Hayneedle raised the largest Series A at $22.0mn and Mizzen Main’s had the smallest Series A at $1.2mn.

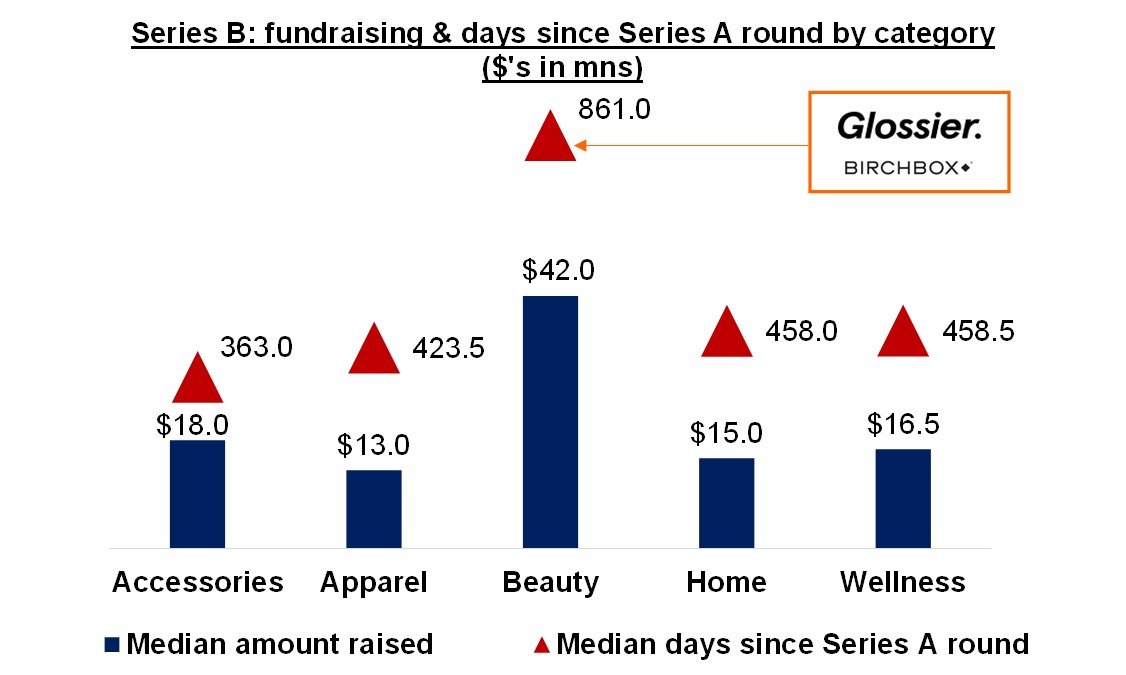

Looking at Series B rounds, Beauty was a huge standout with investments at 2.0x-2.5x larger than any other category due to companies such as Glossier and Birchbox, which could be due to a multitude of things; high margins, good ship to weight ratios, and naturally high repeat rates.

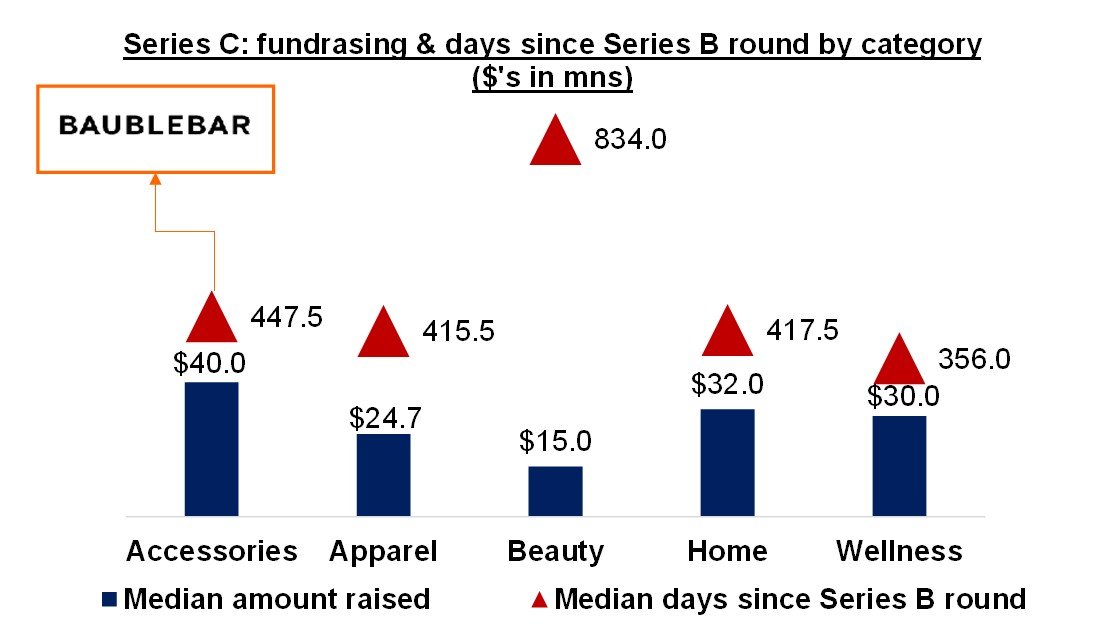

Looking at Series C rounds, Beauty DNVB’s saw investments much lower in comparison and days in between a Series B and C much farther apart. Wellness companies however saw days in between come at the lowest level with around ~355 days, while accessories saw the largest median Series C rounds of $40.0mn.

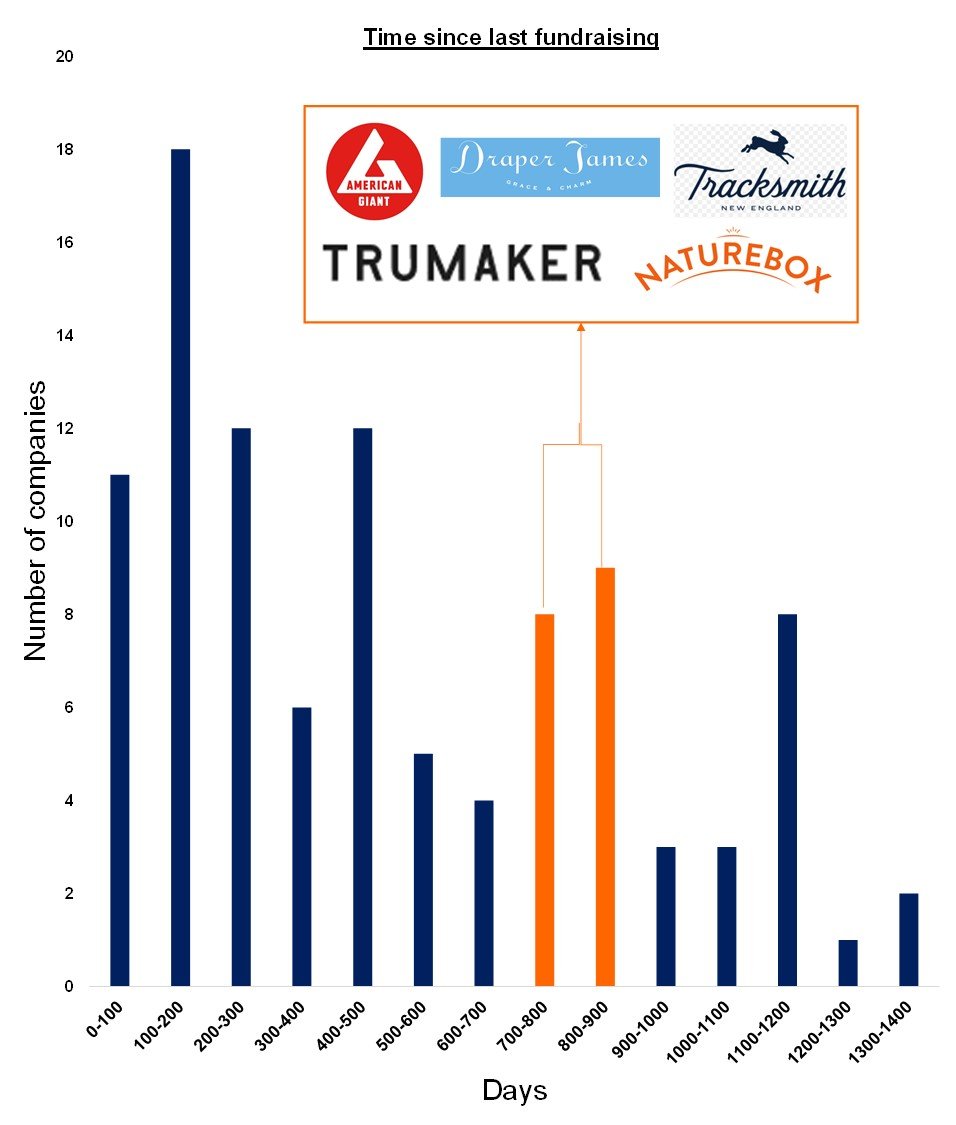

The bubble of DNVBs that haven’t been raised in 700-900 days

We did find a bubble of companies sitting in a range of 700-900 days since their last fundraising – namely companies like American Giant, Draper James, and Trumaker. Who could be at a crossroads of a few things; profitability, extinction, or not looking to give up any more equity. There were also companies who have not raised capital in the past 4 years, including Cuyana (likely doesn’t disclose their funding round), DailyBurn, and J. Hillburn.

Bottom Line: DNVB funding is off from the 2014/2015 levels. The bright shiny object changes from year to year and now it is wellness/home. We have the most comprehensive DNVB database – so e-mail if you’d like to learn more.

Source: Crunchbase, CapIQ

All securities transactions are offered by and conducted through ComCap LLC, a broker-dealer registered with the SEC, and a member of FINRA and SIPC. This communication is for information purposes only and should not be regarded as a solicitation or offer to buy or sell any security or financial instrument and any email received with instructions to purchase or sell securities will not be acted upon. Pursuant to SEC and FINRA regulations, all incoming and outgoing email of persons associated with the broker-dealer are subject to review by the firm’s compliance administrators, principals, and its regulatory agencies.

Copyright © 2022 ComCap LLC member, FINRA & SIPC, All rights reserved.

Subscribe to our newsletter

Sign Up for our monthly newsletter to get the latest news, research reports, and events delivered directly to your inbox